The world of personal finance can feel like navigating a dense fog. You know you have income, you know you have expenses, but the path from one to the other is often obscured. You might check your bank account balance and feel a momentary sense of relief or panic, but that single number tells you very little about your financial health. It’s a snapshot, not the story. To truly understand where you are and, more importantly, where you’re going, you need to turn on the headlights. That’s precisely what a weekly finance dashboard does.

Many people fall into two camps: they either ignore their finances until a bill is overdue (the reactive approach) or they obsessively track every single penny every day (the exhausting approach). A weekly review offers the perfect middle ground. It’s frequent enough to catch problems before they snowball and make course corrections, yet infrequent enough that it doesn’t become a soul-crushing chore. It transforms financial management from a source of anxiety into a routine, empowering habit.

Creating a dashboard isn’t about building complex spreadsheets with pivot tables and macros (unless you’re into that!). It’s about identifying and consistently monitoring a handful of key metrics that give you a clear, high-level view of your financial life. This weekly ritual, which can take as little as 15 minutes, provides the clarity needed to make intentional decisions, reduce stress, and accelerate your progress toward your most important goals. This guide will break down the essential metrics to track on your weekly finance dashboard to cut through the fog and take control of your financial journey.

The Foundation: Why a Weekly Dashboard Changes Everything

Before diving into the “what” to track, it’s crucial to understand the “why.” Why is a weekly cadence so powerful? It’s rooted in the psychology of habit formation and proactive management. Think of it like a fitness journey. Stepping on the scale once a year gives you a shocking result but no actionable data. Stepping on it every single day can lead to obsession over normal fluctuations. But a weekly check-in? That gives you a trend line. It shows you if your efforts from the past seven days paid off and informs your choices for the next seven.

A weekly finance dashboard accomplishes the same thing. It builds momentum. When you see your savings number tick up week after week, it creates a positive feedback loop that encourages you to keep going. When you catch overspending on dining out after just one week, you can adjust your behavior for the next weekend, rather than realizing you blew your entire monthly budget on the 30th. This proactive stance is the difference between being the driver of your financial life and being a passenger holding on for dear life. It reduces financial anxiety because there are no surprises. You develop an intuitive sense of your money’s flow, which is the very definition of financial control.

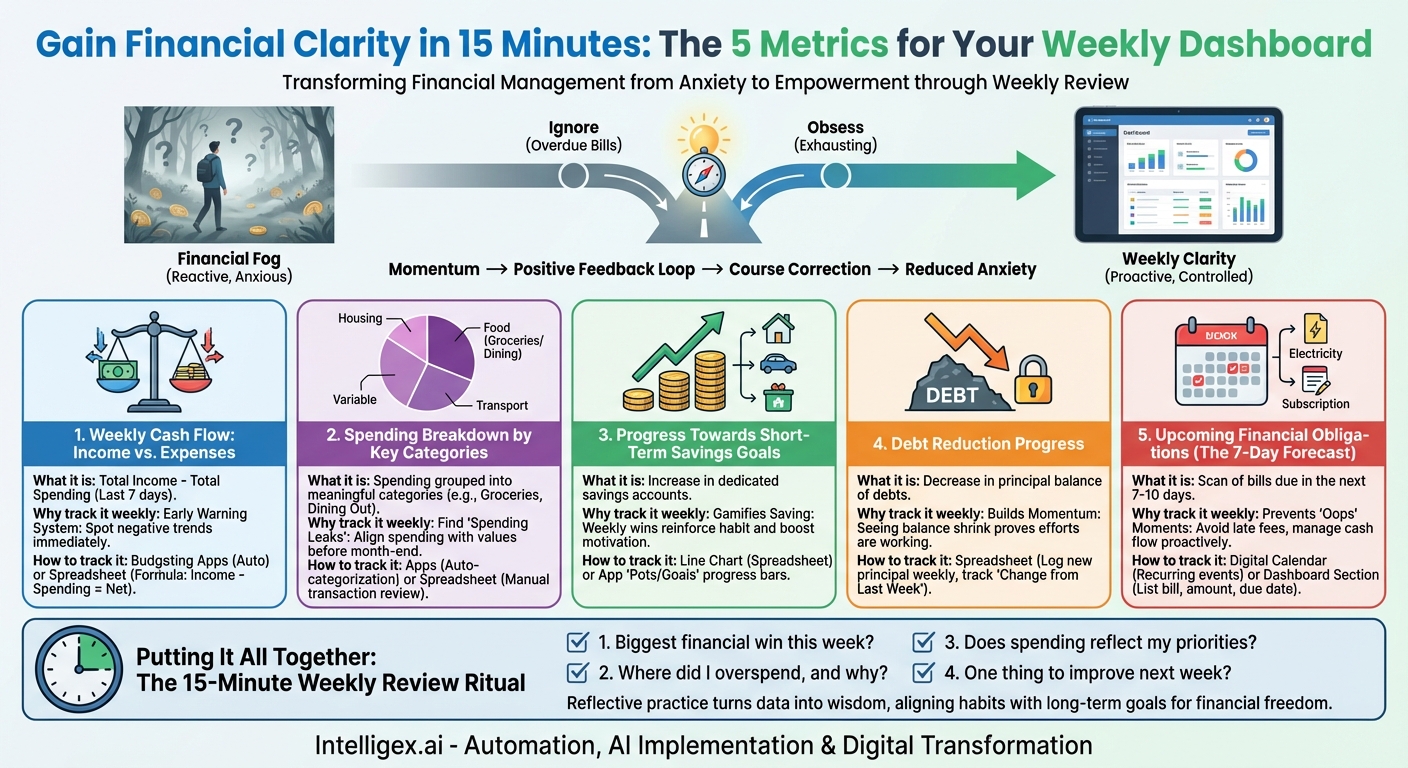

The Core Five: Essential Metrics for Your Weekly Dashboard

Your dashboard should be personal, but there are five universal metrics that provide a comprehensive health check for almost everyone. Start with these, and you can always customize as you become more comfortable with the process.

1. Weekly Cash Flow: Income vs. Expenses

This is the most fundamental metric of all. At its core, personal finance is about ensuring you have more money coming in than going out. A weekly cash flow analysis gives you the most immediate feedback on this principle.

- What it is: A simple calculation of all the money that entered your accounts (paychecks, side hustle income, etc.) versus all the money that left your accounts (bills, groceries, gas, fun) over the last seven days.

- Why track it weekly: It’s your early warning system. A single negative cash flow week isn’t a disaster—maybe a big annual bill was due. But a pattern of negative cash flow weeks is a red flag that signals your lifestyle is more expensive than your income can support. Tracking it weekly allows you to spot this trend immediately.

- How to track it: Most budgeting apps (like Mint, YNAB, or Monarch) do this automatically. If you’re using a spreadsheet, you can create a simple summary: `Total Income This Week – Total Spending This Week = Net Cash Flow`.

2. Spending Breakdown by Key Categories

Knowing your net cash flow is great, but knowing where the money went is where the magic happens. You can’t change what you don’t measure. This metric provides the necessary detail to make informed decisions.

- What it is: A look at your spending grouped into meaningful categories. You don’t need 50 categories. Start with the big ones: Housing, Transportation, Food (split into Groceries and Dining Out), and a general “Variable Spending” bucket for everything else.

- Why track it weekly: This is how you find your “spending leaks.” You might be shocked to discover that your daily coffee habit adds up to $35 a week or that impromptu online shopping sprees are costing you over $100. Seeing these numbers on a weekly basis, rather than as a giant lump sum at the end of the month, makes them more tangible and easier to address. It helps you answer the question, “Did my spending this week align with my values?”

- How to track it: Again, apps are your best friend here as they can automatically categorize most transactions. In a spreadsheet, you’ll need to manually categorize your expenses from your bank statement. It sounds tedious, but for a single week’s worth of transactions, it’s often a quick and insightful exercise.

3. Progress Towards Short-Term Savings Goals

Your dashboard shouldn’t just be about tracking expenses; it should be a source of motivation. Monitoring your progress towards meaningful goals is a powerful way to stay engaged.

- What it is: Measuring the increase in your dedicated savings accounts. This could be your emergency fund, a vacation fund, a down payment fund for a house, or a new car fund.

- Why track it weekly: It gamifies saving. Seeing that balance climb, even by just $50 or $100, is a psychological win. It reinforces the habit of “paying yourself first” and shows you the tangible results of your discipline. A month can feel like a long time, but seeing weekly progress makes the goal feel closer and more achievable, keeping your motivation high.

- How to track it: A simple line chart in a spreadsheet showing the balance over time is incredibly effective. Many banking apps also allow you to create “pots” or “goals” and will show you a progress bar, which is a great visual motivator.

4. Debt Reduction Progress

For those carrying debt, this metric is just as important as savings. Debt can feel like a heavy weight, and tracking your progress is key to staying motivated on the long journey to becoming debt-free.

- What it is: The change in the principal balance of your debts, especially high-interest debt like credit cards or personal loans.

- Why track it weekly: The total balance of a large loan can be demoralizing. But seeing that number shrink week after week, even by a small amount from an extra payment, proves your efforts are working. It shifts your mindset from “this is impossible” to “I am making steady progress.” It highlights the powerful impact of making even small, extra payments whenever possible.

– How to track it: In your spreadsheet, create a section for each debt. Every week, log the new principal balance. The most important column is “Change from Last Week.” Seeing that negative number is a huge win.

5. Upcoming Financial Obligations (The 7-Day Forecast)

A good dashboard doesn’t just look back; it looks forward. Avoiding late fees and the stress of a last-minute cash crunch is a cornerstone of sound financial management.

- What it is: A quick scan of all bills, subscriptions, or other planned financial commitments due in the next 7-10 days.

- Why track it weekly: This simple check prevents “oops” moments. It ensures you have enough cash in your checking account to cover what’s coming, preventing overdraft fees. It also gives you a heads-up on your cash flow for the week ahead. If you see a large car insurance payment is due on Friday, you know to rein in discretionary spending earlier in the week.

- How to track it: This can be as simple as a recurring event in your digital calendar or a dedicated section in your spreadsheet dashboard. List the bill, the amount, and the due date for the upcoming week.

Putting It All Together: The 15-Minute Weekly Review Ritual

A dashboard is useless if you don’t look at it. The key to success is establishing a consistent ritual. Block out 15-30 minutes on your calendar at the same time each week—”Financial Friday” or “Money Sunday” are popular choices. During this time, eliminate distractions and focus solely on your finances.

Your ritual should involve more than just logging numbers. It’s a time for reflection. As you update your dashboard, ask yourself a few simple questions:

- What was my biggest financial win this week? (e.g., “I packed my lunch every day” or “I hit my weekly savings goal.”)

- Where did I overspend, and why? (No judgment, just curiosity. “We had a stressful week, so we ordered takeout more often.”)

- Does my spending reflect my priorities? (If you value health but spent more on fast food than groceries, it’s a sign of misalignment.)

- What is one thing I can do to improve next week? (e.g., “I’ll plan meals for the week ahead” or “I’ll unsubscribe from one marketing email list.”)

This reflective practice is what turns data into wisdom. It’s how you slowly and sustainably align your daily financial habits with your long-term life goals. Your weekly dashboard isn’t a report card for judging your past; it’s a compass for navigating your future.

The journey to financial clarity doesn’t require a finance degree or sophisticated software. It begins with the simple, consistent act of paying attention. By tracking these core metrics weekly, you replace anxiety with awareness and reactivity with intention. You build a system that empowers you to make small, smart decisions every week—decisions that compound over time into a future of financial freedom and peace of mind.

Your Next Read:

Category:

Get a FREE

Proof of Concept

& Consultation

No Cost, No Commitment!